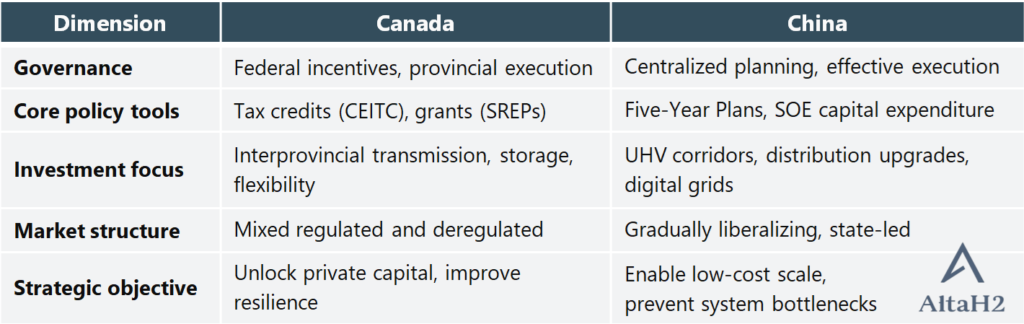

As renewable integration accelerates, Canada’s policy-driven grid upgrades are increasing focus on transmission, storage, and digital intelligence as core drivers of energy competitiveness. Federal budget incentives and large-scale grid modernization plans coincide with China’s accelerating energy transition, together driving demand for transmission infrastructure, energy storage, and next-generation electrical equipment across two of the world’s most advanced power systems.

With rising renewable penetration and structural grid constraints, both systems are scaling up national grid modernization and storage investments. Canada’s 2025 federal budget introduces tax credits and targeted funding to expand renewable integration and interprovincial transmission, while China, shifting from its 14th Five-Year Plan to a more expansive 15th plan, prioritizes ultra-high-voltage (UHV) corridors, distribution network upgrades, and smart grid platforms.

Despite differences in governance, market design, and energy mix, both systems converge on the same imperative: grid capacity, flexibility, and intelligence now determine the pace, resilience, and competitiveness of the energy transition. Together, these developments signal a synchronized grid investment cycle across two globally influential power markets.

Canada: policy-led capital for a clean, multi-jurisdictional grid

Canada’s 2025 Federal Budget and Climate Competitiveness Strategy, released in November 2025, introduced a coordinated package of fiscal incentives aimed at modernizing transmission, scaling grid-connected storage, and unlocking private capital for clean electricity infrastructure. The centrepiece is a 15% Clean Electricity Investment Tax Credit (CEITC) covering low-emitting generation, energy storage, and interprovincial transmission assets.

Crucially, the CEITC expands eligibility beyond traditional utilities to include Crown corporations, municipalities, indigenous-owned enterprises, pension funds, and federal institutions. By broadening the investor base, Canada is addressing a long-standing bottleneck in grid development: capital-intensive projects constrained by fragmented ownership, provincial jurisdiction, and limited risk appetite.

Complementing the tax credit, the Smart Renewables and Electrification Pathways Program (SREPs) remains the federal government’s primary funding vehicle for grid and storage investment. Backed by approximately CAD 4.5 billion through 2035, SREPs targets utility-scale storage, transmission reinforcement, and renewable integration across regions, with an emphasis on system reliability and emissions reduction rather than incremental generation capacity alone.

The budget explicitly recognizes Canada’s structural diversity. Electricity systems are provincially governed, geographically dispersed, and resource-specific, resulting in markedly different grid investment priorities across provinces:

British Columbia operates a predominantly hydroelectric system, with more than 95% of generation from large reservoirs. Its challenge lies in flexibility and interconnection—managing seasonal hydrology, supporting electrification in industry and transport, and strengthening ties with Alberta and the U.S. Pacific Northwest.

Alberta, by contrast, runs Canada’s only fully deregulated electricity market and retains a relatively high share of thermal generation. Rapid wind and solar growth is stressing transmission nodes and increasing price volatility, elevating the role of grid-scale batteries, ancillary services, and transmission reinforcement.

Ontario combines nuclear baseload, hydro, and an expanding storage fleet. It has emerged as Canada’s storage bellwether, anchored by projects such as the 250 MW/1 GWh Oneida Energy Storage facility, the country’s largest battery installation. Storage plays a central role in balancing nuclear-heavy baseload with variable renewables while deferring costly peaking capacity.

Québec operates one of the world’s largest hydro-dominated grids, with roughly 95% renewable generation. Grid investment focuses on transmission expansion, cross-border interconnections, and digitalization to support exports to Ontario and the U.S. Northeast while enabling local electrification.

Across provinces, federal incentives are reshaping grid economics by turning transmission and storage, once treated primarily as regulated cost centers, into investable infrastructure assets with clearer return profiles.

China: system-scale grid expansion under centralized planning

China is entering the 15th Five-Year Plan period (2026–2030) with one of the largest grid investment programs ever undertaken globally. State Grid has announced plans to invest approximately CNY 4 trillion in fixed assets during the period, targeting UHV transmission corridors, cross-regional power transfer, and digital grid platforms to support continued renewable expansion and surging electricity demand.

That demand growth is unprecedented in scale. In 2025, China’s total electricity consumption exceeded 10,000 TWh for the first time—more than double that of the United States and greater than the combined consumption of the European Union, Australia, India, and Japan. Over the past decade, national electricity consumption has nearly doubled, rising from roughly 5,500 TWh in 2015 to today’s level.

The strategic objective of China’s grid investment is scale with coordination. Massive renewable bases, particularly wind and solar installations in the northwest “沙戈荒” (desert, Gobi, and arid) regions, need to be integrated with demand centers along the eastern and southern coasts. To achieve this, State Grid is accelerating deployment of ±800 kV UHV DC and 1,000 kV UHV AC lines, lifting cross-provincial transmission capacity by more than 30% by 2030 relative to end-2025 levels.

China’s grid architecture is anchored by two national operators, State Grid and China Southern Power Grid, and closely integrated with large state-owned generation groups. The five major power producers (Huaneng, Datang, Huadian, China Energy, and SPIC) have all met or exceeded their 14th-plan clean-energy capacity targets. Clean energy now accounts for more than half of installed capacity across major power groups, with SPIC leading at over 74%.

By the end of the 14th Five-Year Plan, State Grid had completed 42 UHV projects, lifting cross-regional transmission capacity to 370 GW. Grid planning follows a principle of “moderate over-anticipation,” with five- to ten-year forward alignment designed to prevent infrastructure from becoming a bottleneck for economic growth, electrification, and decarbonization.

During the 15th plan, investment emphasis is shifting beyond long-distance transmission toward distribution network reinforcement, digital substations, microgrids, and virtual power plants. This reflects the rapid rise of distributed solar, electric vehicles, flexible loads, and ongoing power market reform. In 2025, market-based electricity trading accounted for 64% of total consumption, with green power trading volumes rising more than 38% year-on-year. Grid modernization in China is increasingly about real-time coordination at the edge of an ultra-large, market-enabled system.

Key technologies enabling infrastructure

As renewable adoption continues to increase, two converging technology domains underpin grid and storage investment in both markets.

I. High-capacity transmission and interconnection

Canada already generates about two‑thirds of its electricity from renewables, with hydro accounting for roughly 57%. The challenge is geographic mismatch rather than a supply shortage. Federal funding is therefore directed toward interprovincial corridors, advanced conductors, power electronics, and digital controls that enable clean power to flow from resource-rich provinces to load centers.

In China, UHV transmission plays a structurally similar role at far greater scale. UHV corridors enable thousands of megawatts to move over distances exceeding 2,000 kilometers with minimal losses, forming the backbone of China’s national power-balancing strategy.

II. Energy storage at system scale

Grid-level storage is rapidly moving from demonstration to deployment. In Canada, federal projections indicate that grid-connected storage capacity above 1 MW could more than double by 2030, reaching nearly 2.8 GW if announced projects proceed. Storage increasingly underpins frequency regulation, peak shaving, and renewable firming.

China continues to scale pumped-storage hydropower while accelerating deployment of new-type energy storage (NTES) at both utility and distribution levels. Storage assets are increasingly integrated with digital platforms, enabling participation in spot markets, ancillary services, and virtual power plant aggregation.

Commercial scale and competitiveness

The convergence of policy support and infrastructure need is creating substantial commercial opportunity across the power value chain.

In Canada, the CEITC and SREPs are expected to catalyze multi-billion-dollar investment flows, drawing institutional capital into grid assets that were previously constrained by regulatory complexity. Utilities benefit from improved system reliability, while equipment manufacturers face rising demand for transformers, power electronics, control software, and grid-scale batteries

China’s CNY 4 trillion grid investment plan represents one of the largest addressable markets globally for electrical equipment, digital grid solutions, and energy storage systems. Domestic scale and centralized procurement continue to drive rapid cost reductions, reinforcing China’s competitive position in grid infrastructure and power-electronics manufacturing.

Outlook and strategic implications

The parallel acceleration of grid investment in Canada and China reflects a broader, systems-level shift. Grid modernization and energy storage are no longer ancillary to clean generation; they have become core enablers of electrification, decarbonization, and energy security.

For policymakers, the focus is moving from capacity targets to system performance. For investors and suppliers, opportunity increasingly lies in flexibility, digitalization, and system integration rather than standalone assets. For utilities, grid intelligence is becoming as critical as physical infrastructure.

As Canada deploys policy-led incentives to mobilize capital and China advances system-scale grid expansion through centralized planning, both economies illustrate distinct yet complementary pathways for accelerating the clean energy transition—united by a shared recognition that grid transmission and intelligence is emerging as the decisive arena of the next energy era.