New Canada–China trade agreements and UK–China technology partnerships are accelerating the integration of EV and smart-grid value chains, with direct implications for Canada’s automotive sector and energy transition strategy.

In January, Canada agreed to allow up to 49,000 Chinese-built electric vehicles into its market annually under a reduced tariff regime, while London-based Octopus Energy announced a major joint venture to enter China’s renewable energy market. These developments coincide with the implementation of China’s mandatory EV energy-consumption standard on January 1, 2026, which tightens efficiency requirements and reinforces China’s influence over global EV technology trajectories, cost curves, and supply chains.

Clean-tech diplomacy

In January 2026, during the Canadian Prime Minister’s official visit to China, the two countries established a “new strategic partnership” spanning trade, energy, and clean tech cooperation. A central outcome was an agreement permitting the import of up to 49,000 Chinese-manufactured EVs per year at a most-favoured-nation tariff rate of 6.1%.

The import cap, equivalent to roughly 3% of Canada’s annual new-vehicle market, reflects pre-restriction trade volumes and is widely expected to expand over time. While limited in the near term, the arrangement creates a regulated entry channel for Chinese EV manufacturers and signals Canada’s attempt to balance industrial protection, affordability, supply chain diversification, and climate objectives.

Simultaneously, during the UK Prime Minister’s January visit to China, Octopus Energy announced a joint venture focused on renewable power trading in China’s rapidly reforming electricity markets. The venture targets up to 140 TWh of green electricity trading annually by 2030, leveraging British expertise in digital energy platforms to operate within the world’s largest power system. It also reflects China’s growing openness to foreign participation in electricity-market services, as distinct from asset-heavy generation ownership.

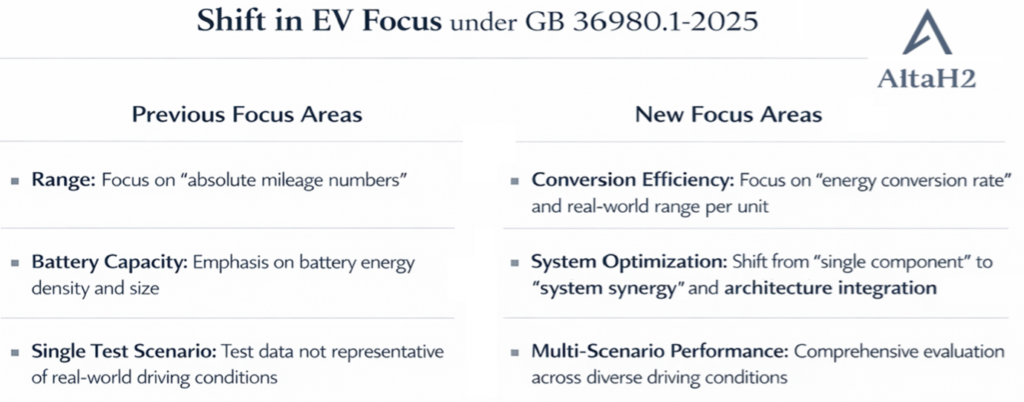

China’s new EV standards

These commercial moves coincide with the introduction of China’s new national EV efficiency standard GB 36980.1-2025: Limits of Energy Consumption for Electric Vehicles – Part 1: Passenger Cars, which took effect on January 1, 2026 and introduces a more comprehensive, system-level approach to vehicle energy performance.

The new EV standard represents a structural shift from component-level efficiency benchmarks to system-level vehicle performance metrics. This shift responds to a core industry constraint: as improvements in battery energy density have plateaued, simply adding battery capacity to extend driving range has become both economically inefficient and technically limiting.

Under the mandatory standard, energy-consumption limits tighten by approximately 11% compared with the previous requirement. For a two-ton electric passenger vehicle, maximum allowable energy consumption is capped at 15.1 kWh per 100 km. Holding battery capacity constant, compliance is expected to increase average driving range by roughly 7%, achieved through efficiency gains rather than larger battery packs.

Technically, the standard integrates requirements across thermal management, power electronics, regenerative braking, drivetrain efficiency, and vehicle mass optimization. It explicitly links overall vehicle efficiency to multi-system coordination rather than isolated component performance. This shift is particularly relevant in cold-climate conditions, where inefficient cabin heating and battery thermal control have typically undermined EV range and consumer confidence, an issue of direct relevance to the Canadian market.

Market scale, competition, and policy alignment

Together, Canada’s evolving trade strategy, China’s tightening efficiency standards, and the UK’s expansion of digital energy platforms highlight a broader realignment in global EV and renewable-energy competition. Market access, efficiency regulation, and digital coordination are increasingly intertwined, shaping how value is created and captured across borders. Against this backdrop, the implications for Canada unfold across vehicles, standards, platforms, and adoption dynamics.

I. Canadian EV imports

The Canada–China EV agreement opens a controlled but strategically meaningful pathway for Chinese manufacturers to participate in the Canadian market. While 49,000 units per year represents a modest share today, projected market growth of around 6% annually, combined with preferential tariffs, establishes a durable foothold for Chinese brands.

The implications are material: increased price competition, expanded consumer choice, and rising pressure on incumbent OEMs and dealer networks—particularly in the sub-CAD 35,000 EV segment, where affordability remains a key barrier to mass adoption in Canada.

For Canadian businesses and EV dealers, this shift may also catalyze new commercial models that integrate vehicles, energy, and digital services, blurring traditional boundaries between automakers, utilities, and software providers. One reference point is Octopus Energy’s earlier collaboration with BYD.

Launched in 2021 in the UK, its “zero-upfront EV package” allowed consumers to access an electric car for £299 per month, with vehicle use, charging, and electricity bundled into a single service. Octopus retained ownership of the vehicle, monetizing it through vehicle-to-grid (V2G) services—generating £40–65 per vehicle per month—while also receiving sales incentives from automakers. The model reframed EVs as “batteries on wheels,” illustrating how energy and transport can converge into a unified value proposition—an approach that could gain traction in Canada as grid-flexibility needs and EV penetration rise.

II. China’s EV standard

For global automakers, China’s mandatory energy-consumption limits introduce new engineering and compliance thresholds. Export-oriented manufacturers operating in China must now align vehicle architectures with China’s system-level efficiency logic, increasing design complexity but also accelerating global technology convergence.

For non-Chinese OEMs supplying the Canadian market, the effects are likely to be pronounced. To remain performance- and efficiency-competitive against Chinese imports, manufacturers may need to integrate advanced thermal-management systems, next-generation power semiconductors, and lightweight materials earlier in product-development cycles, raising near-term R&D intensity while improving long-term efficiency, regulatory resilience, and margin structure.

III. UK energy platforms

Beyond vehicles, competitive dynamics are increasingly shifting toward digital infrastructure and market-orchestration capabilities. On the energy-system side, Octopus Energy’s China joint venture will deploy algorithmic trading platforms and AI-driven forecasting tools, similar to those used in European real-time power markets, into China’s emerging spot markets.

This model could also provide a reference point for the Canadian market. By combining demand prediction, price optimization, and grid-level analytics, the platform aims to improve renewable utilization, enhance system flexibility, and reduce curtailment as wind and solar capacity continue to scale.

IV. EV market penetration

According to Statistics Canada, zero-emission vehicles (ZEVs, including BEVs and PHEVs) accounted for roughly 18.3% of new vehicle registrations nationwide in late 2024, reflecting steady progress. Québec, by contrast, reached approximately 30.9% ZEV penetration, leading provincial adoption and underscoring significant regional variation.

Canada’s experience suggests that strong incentives and charging infrastructure can accelerate EV uptake, but recent changes to rebate policies have introduced volatility in 2025. Crossing the 20% penetration threshold is widely viewed as a critical inflection point toward mass-market adoption.

China’s experience illustrates how rapidly this transition can unfold. In its passenger vehicle market, electric-car penetration rose from 25% to 50% in just 16 months, underscoring the speed at which adoption can scale once cost, infrastructure, and policy dynamics align.

A similar pattern is now evident in China’s heavy-duty electric truck market. Penetration increased from 0.7% in 2021 to 5.2% in 2022 and 5.5% in 2023, before reaching an inflection point in 2024, when full-year penetration climbed to 13.6%. In 2025, annual penetration surged to 29%, with monthly penetration surpassing 50% in December—highlighting the non-linear nature of electrification once industrial scale and regulation converge.

Value chains and global competition

Strategically, Canada’s EV import policy signals an effort to diversify supply chains, with implications for trade governance, investment decisions, and the structure of Canada’s automotive ecosystem. Concurrently, China’s EV efficiency mandate—combined with its scale in battery and vehicle manufacturing—reinforces its position as a central node in global decarbonization value chains.

For Canadian companies, this creates opportunities to pair “China’s hardware” with “Canadian software”: combining cost-competitive Chinese batteries and vehicles with domestic strengths in renewable-energy integration, digital platforms, grid optimization, and energy analytics. Such combinations could support differentiated business models in fleet management, smart charging, V2G aggregation, and distributed energy services, positioning Canada higher in the EV value chain beyond assembly and retail.

More broadly, the Octopus Energy example underscores a shift in competitive advantage toward firms that manage complexity through data rather than ownership of physical assets. Companies with advanced digital trading, optimization, and AI capabilities increasingly shape energy markets by orchestrating flows of power, data, and flexibility across interconnected systems.

Taken together, these developments illustrate how trade diplomacy, regulatory standards, and private innovation are converging to reshape competition across EV and clean-energy markets. For automakers, utilities, and energy-technology firms, success over the next decade will depend on aligning products, platforms, and partnerships with a rapidly evolving global regime of efficiency regulation and market access.