How tariff relief on canola and calibrated EV access align trade policy with industrial competitiveness and low-carbon fuels in Western Canada

On January 16, Canada officially announced a new strategic partnership with China spanning energy, agri-food, and trade—an agreement that lowers key barriers to Canadian exports while opening the door to joint investment in clean technologies.

The deal arrives at a critical moment for Canada’s economy, as global trade patterns shift and the decarbonization of transport and industry accelerates. By pairing tariff relief for agricultural commodities with carefully calibrated access for Chinese electric vehicles (EVs), alongside an explicit commitment to clean energy collaboration, Canada is positioning trade policy as a lever for long-term industrial competitiveness rather than short-term political signalling.

A targeted trade re-arrangement with outsized gains

At the centre of the announcement is a substantial reduction in Chinese tariffs on Canadian canola seed. By March 1, 2026, China is expected to lower combined tariffs to approximately 15%, down from roughly 85% today. For Canadian producers, this represents a structural reset rather than a marginal adjustment: China is a CAD 4 billion annual market for canola seed, and the tariff reduction effectively restores access to one of Canada’s most important export destinations.

Equally significant is interim relief for downstream products. Canadian canola meal and peas are expected to avoid relevant anti-discrimination tariffs from March 1, 2026 through at least the end of that year, providing stability for processors and exporters seeking predictable market access. Canola meal typically accounts for 30–35% of the total revenue from a tonne of crushed seed, making tariff certainty on meal nearly as commercially important as access for the seed itself.

In parallel, Canada will allow up to 49,000 Chinese EVs to enter its market annually at the most-favoured-nation tariff rate of 6.1%. This volume represents less than 3% of Canada’s annual new vehicle sales, limiting domestic market disruption while signalling openness to clean mobility trade.

Federal officials estimate the package could unlock nearly CAD 3 billion in new export orders and catalyze meaningful Chinese joint-venture investment in Canada within three years. Canada has also set a clear objective to increase exports to China by 50% by 2030, with growth anchored in agri-food, clean energy, technology, and wood products.

In addition, the two countries signed a Canada–China Economic and Trade Cooperation Roadmap, comprising eight priority areas and 28 specific initiatives. These span traditional sectors such as energy and agriculture, support for small and medium-sized enterprises (SMEs), and emerging fields including new materials, advanced manufacturing, clean energy, and green products.

From trade policy to fuel molecules: canola’s role in SAF

While the headline figures focus on agri-food exports, the deeper strategic importance lies in how tariff relief on canola strengthens Canada’s low-carbon fuel value chain. Canola oil is already an established feedstock for renewable diesel and sustainable aviation fuel (SAF) production in North America, owing to its high oil yield, favourable fatty-acid profile, and compatibility with the hydroprocessed esters and fatty acids (HEFA) pathway—the dominant commercial SAF technology today.

Lower tariffs improve farm-gate economics and increase throughput certainty for crushers, creating a more scalable and reliable feedstock supply for biofuel producers. Just as important, tariff relief on canola meal materially improves SAF project bankability. Because meal sales can account for up to 35% of cost recovery for crushed seed, secure access to the Chinese market effectively underwrites a significant portion of feedstock economics. For SAF developers, this reduces revenue volatility and strengthens the credit profile of integrated crushing-and-fuel projects.

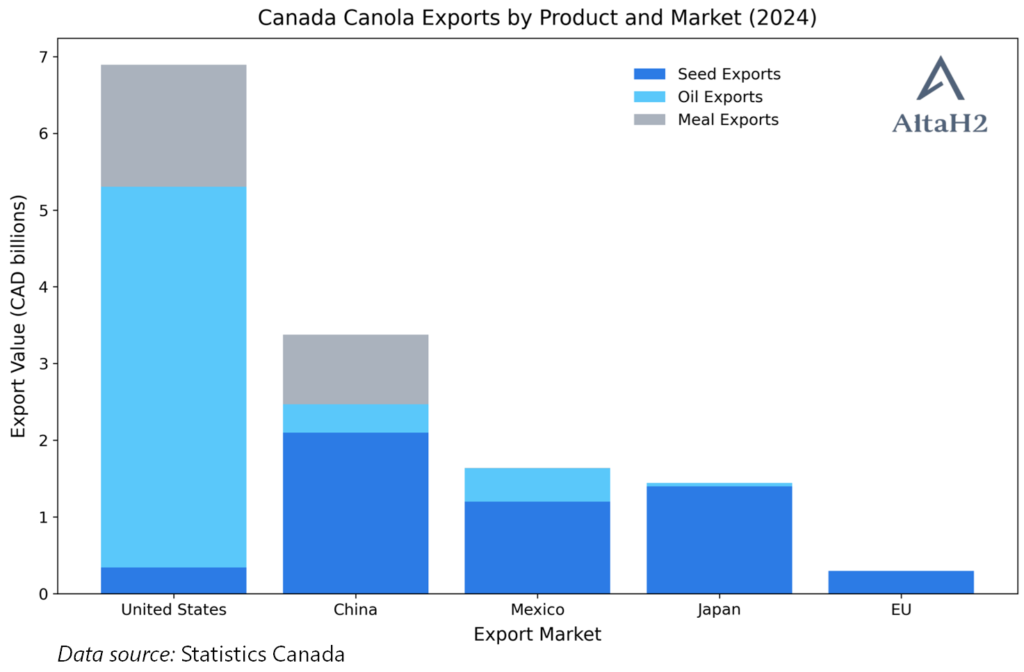

As shown in the diagram above, Canada’s 2024 canola exports to China totalled approximately CAD 3.4 billion, with roughly two-thirds attributable to seed and about one-quarter to meal. The new tariff arrangement creates a pathway for Canada to export higher-value-added canola meal to China while directing canola oil into domestic SAF production for global markets—shifting the export mix away from raw commodities toward higher-margin, climate-aligned products.

In this way, trade policy becomes an upstream enabler of downstream decarbonization, directly linking Prairie agriculture to global aviation climate objectives.

This linkage is increasingly important as global SAF demand accelerates. The International Air Transport Association (IATA) estimates global SAF demand could reach 30–40 billion litres annually by 2030 under stated policies, compared with global production of well under one billion litres today. Feedstock availability and cost stability remain among the most binding constraints.

By restoring access to China’s market for both canola seed and meal, Canada materially strengthens the economics of expanded oilseed production—supporting domestic SAF projects competing for capital in a cost-sensitive, policy-driven environment.

Bridging to SAF: policy alignment meets industrial execution

Canada’s federal and provincial climate frameworks are increasingly aligned with aviation decarbonization. The Clean Fuel Regulations (CFR) create tradable credit value for low-carbon fuels, while provincial incentives and investment tax credits reduce capital risk for large-scale biofuel facilities.

Against this backdrop, the canola tariff breakthrough reflects a rare confluence of trade, climate, and industrial policy. The logic is straightforward:

Harmonized trade → greater agricultural scale → more competitive and de-risked feedstock → bankable SAF projects → exportable low-carbon fuels and technologies.

This virtuous cycle is most visible in Western Canada, where agricultural abundance, energy expertise, and infrastructure depth intersect.

Western Canada—and Alberta in particular—stands out

Western Canada has long underpinned the country’s resource economy. Increasingly, it is also emerging as a proving ground for low-carbon industrial transformation. Alberta combines three advantages that few jurisdictions can match: large-scale biomass availability, world-class energy engineering and EPC capabilities, and globally leading carbon capture, utilization, and storage (CCUS) technologies.

Calgary sits at the centre of this ecosystem. Widely regarded as Canada’s energy capital, the city brings deep expertise in project finance, engineering, and large-scale process execution—capabilities readily transferable from the traditional oil and gas sector to SAF development.

In 2025, Calgary launched the Calgary Regional Hydrogen Hub (CRH2), positioning SAF as a key pillar of its broader low-carbon hydrogen and fuels strategy.

Calgary’s SAF playbook

This policy-industrial alignment is now translating into concrete project execution. In 2024, ABB announced a strategic collaboration with Cap Clean Energy, a Calgary-based company focused on next-generation aviation fuels, to integrate ABB’s automation, electrification, and digital optimization technologies into advanced biofuel facilities.

The technical focus is on producing ultra-low-carbon SAF from non-food crop feedstocks, with lifecycle emissions reductions exceeding 90% relative to conventional jet fuel. Facility designs allow for carbon capture integration, enabling the potential for net-negative emissions—an increasingly valuable attribute as airlines, regulators, and financiers scrutinize full lifecycle performance.

Cap Clean Energy’s planned SAF facility is designed for approximately 3.2 million barrels of annual output, placing it among the larger announced SAF projects in North America, with initial production expected in 2027. At that scale, the project would make a meaningful contribution to regional supply, supporting both domestic airlines and export markets.

Automation and digital controls are central to cost competitiveness. ABB’s systems aim to maximize yield efficiency, reduce energy intensity, and ensure consistent product quality—critical factors in a market where SAF still costs two to five times more than conventional jet fuel without policy support.

Airlines, offtake, and early demand signals

Supply alone does not create a market. Demand signals are equally critical. In 2024, Calgary-based WestJet purchased its first SAF volumes from Shell Aviation. While modest in scale, the transaction was strategically important—demonstrating airline willingness to begin integrating SAF into operations and validating early offtake pathways for domestic producers.

WestJet has committed to net-zero emissions by 2050, in line with global airline targets. Incorporating SAF into operations demonstrates operational readiness and helps de-risk future long-term offtake agreements, often a prerequisite for project financing.

Shell Aviation’s involvement highlights another commercial reality: SAF markets are global, but logistics, certification, and blending requirements remain complex. Partnerships with established fuel suppliers help airlines navigate ASTM certification processes and airport fuel infrastructure constraints.

Together, these early moves indicate that Canada’s SAF ecosystem is transitioning from concept to commercialization.

From trade re-arrangement to clean energy leverage

The Canada–China partnership reframes trade not as a zero-sum contest, but as a platform for industrial scaling. While EV imports have drawn public attention, the longer-term strategic opportunity may lie in clean energy collaboration and agri-based fuels.

China remains the world’s largest aviation market by long-term passenger growth potential and a major source of clean energy investment. Joint ventures in SAF technology, feedstock processing, and carbon management could follow—particularly if Canada achieves its objective of increasing exports to China by 50% by 2030.

For Western Canada, the implication is strategic optionality. By anchoring SAF production in a region with CCUS capacity, skilled labour, and agricultural scale, Canada positions itself not only as a supplier of low-carbon fuels, but also as an exporter of integrated decarbonization solutions.

What began as a pragmatic trade reset with China may ultimately accelerate Canada’s role in one of the world’s hardest-to-abate sectors. By linking canola fields to jet engines—and trade policy to climate execution—Canada is advancing a model in which agriculture, energy, and geopolitics increasingly converge.-to-abate sectors. By linking canola fields to jet engines—and trade policy to climate execution—Canada is advancing a model in which agriculture, energy, and geopolitics increasingly converge.